Pre-Invoice Financing

Often you may need capital prior to being able to issue an invoice. Republic has three products that are specifically designed for this purpose.

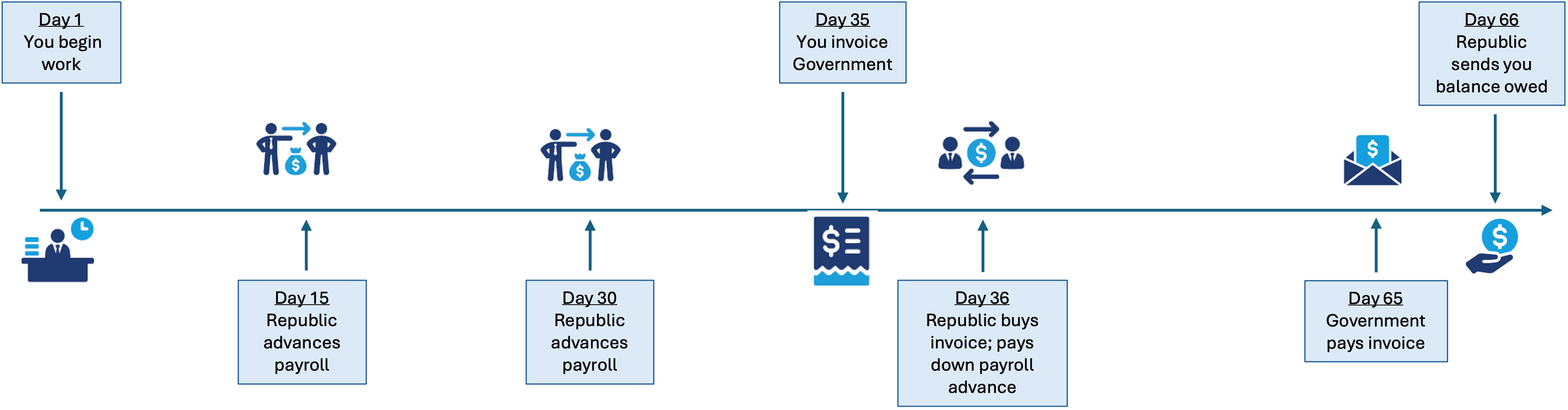

Unbilled/Mobilization/ Payroll Financing

This product provides financing for work you have performed, but not yet billed.

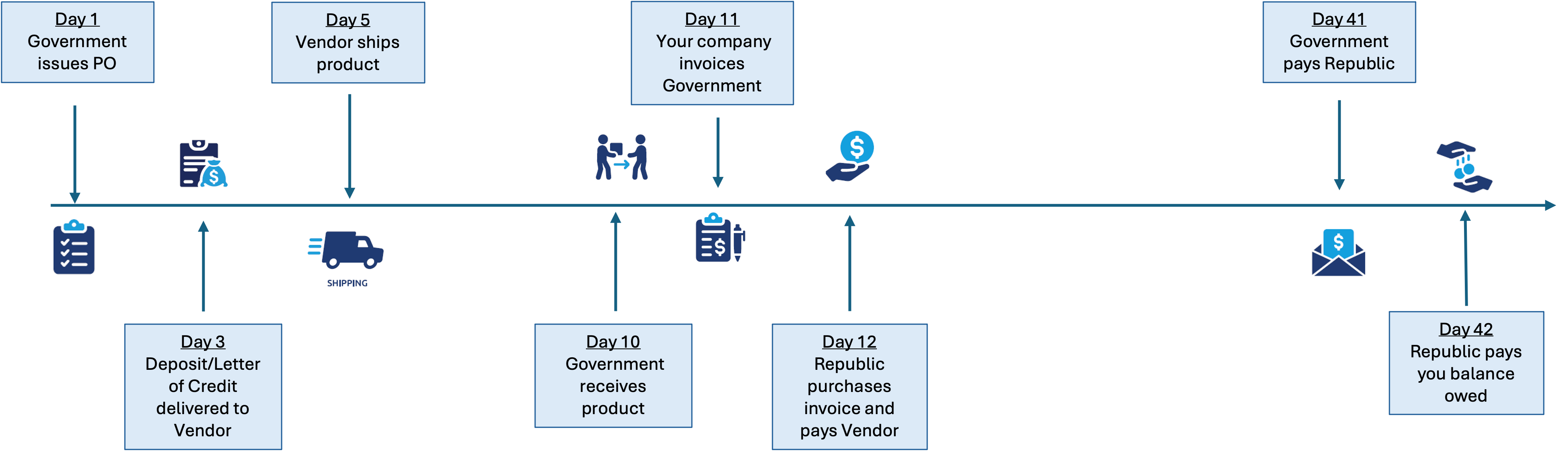

Purchase Order Financing

This product provides your vendor certainty of payment before shipping goods or products related to a government purchase order.

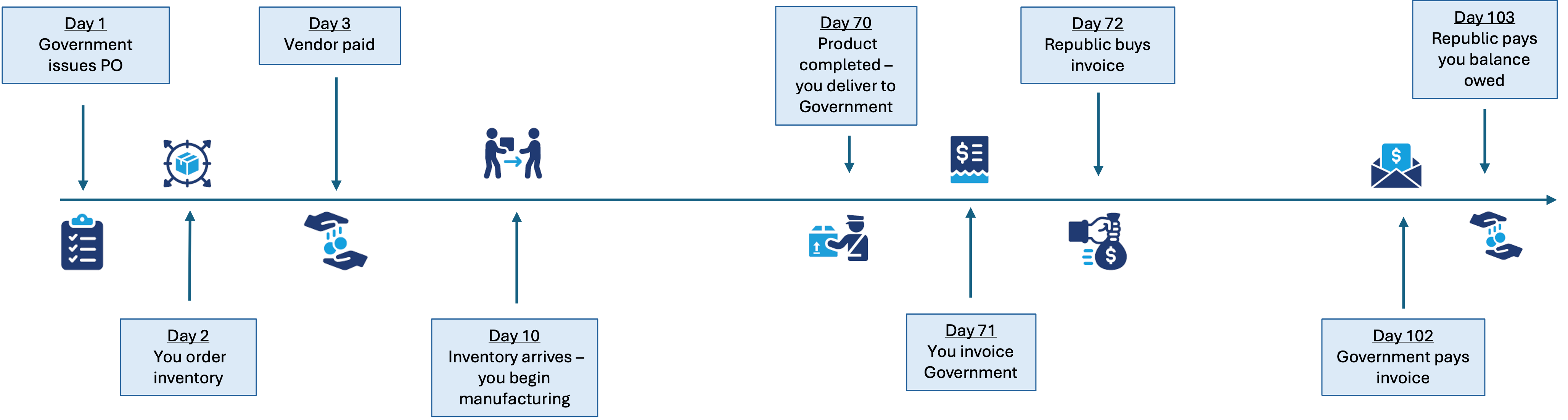

Work-in Process Financing

This product finances inventory and labor related to your contract.

Find out how we can help.